Tom Talks Taxes - March 23, 2023

How to undo married filing jointly tax returns

Tax professionals often say, “you can make up, but you can’t break up,” about a married filing jointly (MFJ) tax return. Like all adages, it is true in most circumstances, but not all: there are four ways to undo a previously filed MFJ return.

If a taxpayer is unsure that they want to file an MFJ return, they should file a married filing separately (MFS) return and then later amend to MFJ once a decision is made. This is much easier than undoing an already filed MFJ return. Per §6013(b)(2)(A), the MFJ election generally must be made no later than three years from the unextended due date of the return.

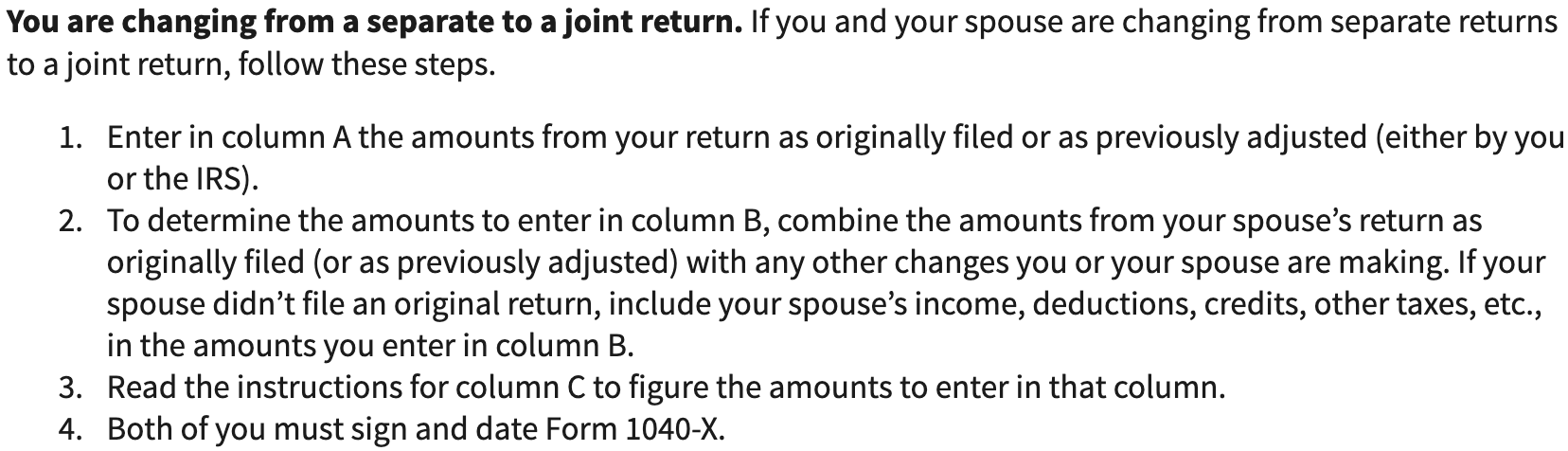

The joint election is made on Form 1040-X, Amended U.S. Individual Income Tax Return. The Form 1040-X instructions provide the following information:

Only one amended return must be filed; whoever will be the taxpayer on the joint return has their return amended to include the spouse’s tax items. The IRS will reverse the spouse’s separate return as part of this process. It can be helpful to have an IRS account transcript for both taxpayers before submission of the amended return, just in case there is an error in making all the account changes.

Please note that the COVID-19 postponements did not affect this provision (it is not listed in Rev. Proc. 2018-58); therefore, for a 2019 MFS return, the amended return electing an MFJ return must be received on or before April 18, 2023.

The four ways a taxpayer can undo an MFJ tax return are:

File a superseding return on or before the unextended due date,

Have the marriage annulled,

Show that the MFJ return was signed under duress, or

Show the MFJ return was not signed by both taxpayers.

Superseding return. A superseding return is an original or amended return filed prior to the due date or extended due date on the return. To undo the joint election, Internal Revenue Manual (IRM) 21.6.7.4.10 states that the superseding return must be filed prior to the unextended due date. The IRS recently added a superseding return electronic checkbox on Form 1040 and the ability to e-file Form 1040X with a filing status change.

Annulment. An annulment is different than a divorce in that the marriage is treated as if it never occurred. State law governs when an annulment is available. Common circumstances include duress, lack of consent, mental illness, and fraud.

If a taxpayer’s marriage is annulled, Rev. Rul. 76-255 states that a taxpayer can amend any MFJ returns open under the relevant statutes of limitation (assessment or refund) to single or head of household. There is no statute of limitations to request abatement of an unpaid tax liability, so this is a way to potentially sever someone from tax debts for which they have joint and several liability on an MFJ return. Internal Revenue Manual 21.6.1.5.5(2) states that proof of annulment should be attached to each amended tax return.

Duress. According to Treas. Reg. §1.6013-4(d), if an individual establishes that he or she signed an MFJ return under duress, the return is not an MFJ return, and the individual is not jointly and severally liable. In Stanley v. Comm., 81 T.C. 634 (1983), the Tax Court held that a spouse that is disavowing the signing of an MFJ return must show that they

Were unable to resist demands to sign the return, and

Would not have signed the return except for the constraint applied to their will.

Dual Signature. According to Treas. Reg. §1.6013-1(a)(2), an MFJ return must generally be signed by both spouses unless the return is being made by an agent of one or both spouses. In Carroro v. Comm., 29 B.T.A. 646 (1933), the Tax Court held that the absence of one spouse's signature does not preclude MFJ return status if one spouse gave “tacit consent” to file an MFJ return.

It is difficult to demonstrate a spouse did not give tacit consent; however, the timely filing of their own separate tax return is a strong fact favoring that consent was not given. Additional factors to be considered include MFJ filing history and whether the nonsigning spouse’s tax items were included on the joint tax return.

Join the Conversation

If you are a paid subscriber, you can discuss anything related to MFJ returns in the comments section. Please keep the discussion related to this topic.

If you are a paid subscriber looking to ask an unrelated question, please post it to the most recent Ask Tom Anything post.

Filing Status Education

I have a 2 CE/CPE class on Filing Status: Rules & Planning for Compass Tax Educators. You can purchase it today and take it after filing season (or when you need a break from tax returns).

Thanks Tom, I have a return coming up, exactly like this.