An Overview of the Enhanced Senior Deduction

This deduction can help lower tax liabilities for most seniors age 65+

§70103 of the One Big Beautiful Bill Act (OB3 Act) added new §151(d)(5)(C) to create a new deduction of up to $6,000 for an individual age 65 or older by the end of the tax year ($12,000 total on a joint return if both taxpayers are 65 or older).

While politicians refer to this provision as “no tax on Social Security,” the deduction is unrelated to a taxpayer’s receipt of Social Security benefits.

The senior deduction does not reduce AGI but does reduce taxable income; it can be claimed regardless of whether the taxpayer itemizes deductions. The deduction is available for tax years 2025 through 2028 on Schedule 1-A, Additional Deductions.

Age Determination

For purposes of determining a taxpayer’s age, they are considered to have attained their age on the day before their actual birthday. If a taxpayer died in 2025, they must have lived until they attained age 65. See the 2025 Form 1040 Instructions, p. 110.

Example. Abel was born on February 14, 1960, and died on February 13, 2025. He is considered age 65 at the time of death and would qualify for the senior deduction for tax year 2025. However, if Abel died on February 12, 2025, he would not have attained age 65 in tax year 2025 and would not qualify for the senior deduction.

Deduction Phase-Out

The $6,000 deduction is reduced by 6% of modified adjusted gross income (MAGI), to the extent it exceeds $75,000 ($150,000 on a joint return), and is not reduced below $0. On a joint tax return with two individuals aged 65 and older, each $6,000 amount is phased out separately, so the deduction is completely phased out at $250,000 AGI. MAGI is AGI plus amounts excluded under §911, §931, or §933.

Example. In tax year 2025, Gerald is 88, and Samantha is 62, and they filed a joint return with MAGI of $175,000. Their senior deduction is $4,500, which is $6,000 less $1,500 (6% of $25,000, the amount their MAGI exceeds $150,000).

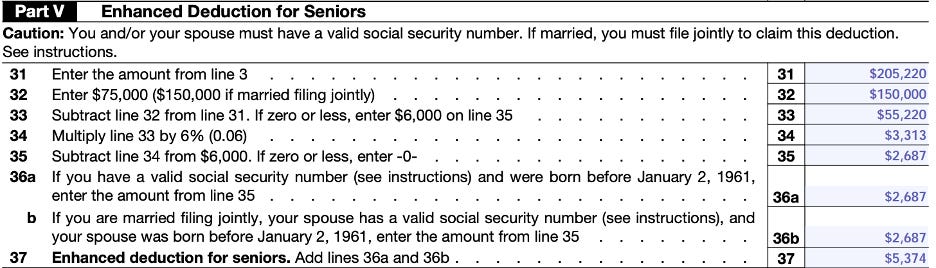

Example. Troy and Harris are married and file a joint return. In tax year 2025, Troy is 68 and receiving Social Security benefits, and Harris is 65 and not receiving Social Security benefits. Their 2025 MAGI is $205,220. They both qualify for the senior deduction at a reduced amount, even though Harris has not yet applied for Social Security benefits. Their combined senior deduction is $5,374 as calculated below:

Additional Deduction Requirements

The taxpayer must include their SSN on their tax return. The SSN must be valid for employment and issued before the due date of the tax return (including extensions). The omission of the SSN is treated as a mathematical or clerical error for which the IRS has the authority to adjust the return without a notice of deficiency being issued.

If married, the taxpayer must file a joint tax return to claim the deduction; it is not available on a married filing separately return.

2026 Tax Planning Considerations

If the taxpayer’s MAGI will limit or eliminate the senior deduction, consider strategies to reduce the 2026 MAGI (e.g., accelerate deductions, defer income, retirement distribution planning). Taxpayers greater than age 70.5 should consider tax-free qualified charitable distributions (QCDs) to meet their charitable goals and/or required minimum distribution (RMD) requirements.

The taxpayer’s AGI in tax year 2026 will affect their Medicare IRMAA surcharges in tax year 2028. While the 2028 IRMAA thresholds are not known, they will most likely overlap with the upper end of the senior deduction phase-out range.

If a taxpayer’s income is insufficient to use all the deductions that they are entitled to (e.g., standard/itemized deductions, senior deduction), they should consider accelerating income to tax year 2026 to utilize these deductions (e.g., Roth conversions, traditional IRA distributions, capital gain harvesting). Be careful to track the effect on AGI to avoid losing any positive tax attributes.

Join the Conversation

If you are a paid subscriber, you can talk about this topic in the comments section. Please keep the discussion related to this edition’s topic.