Tom Talks Taxes - January 11, 2023

Skyrocketing IRS interest rates have important tax effects

The rapid increase in overall interest rates during 2022 has led to a significant increase in IRS interest rates, both on overpaid and underpaid taxes.

Under §6621(a), the underpayment rate is generally the federal short-term rate plus 3%, while the overpayment rate is generally the federal short-term rate plus 3% (2% in the case of a corporation). Interest is compounded daily.

For individuals, the 2023 1st quarter rate is 7%; the same quarter in 2022 was 3%. If the Federal Reserve continues to raise interest rates during 2023, the IRS rate could go to 8% or 9%.

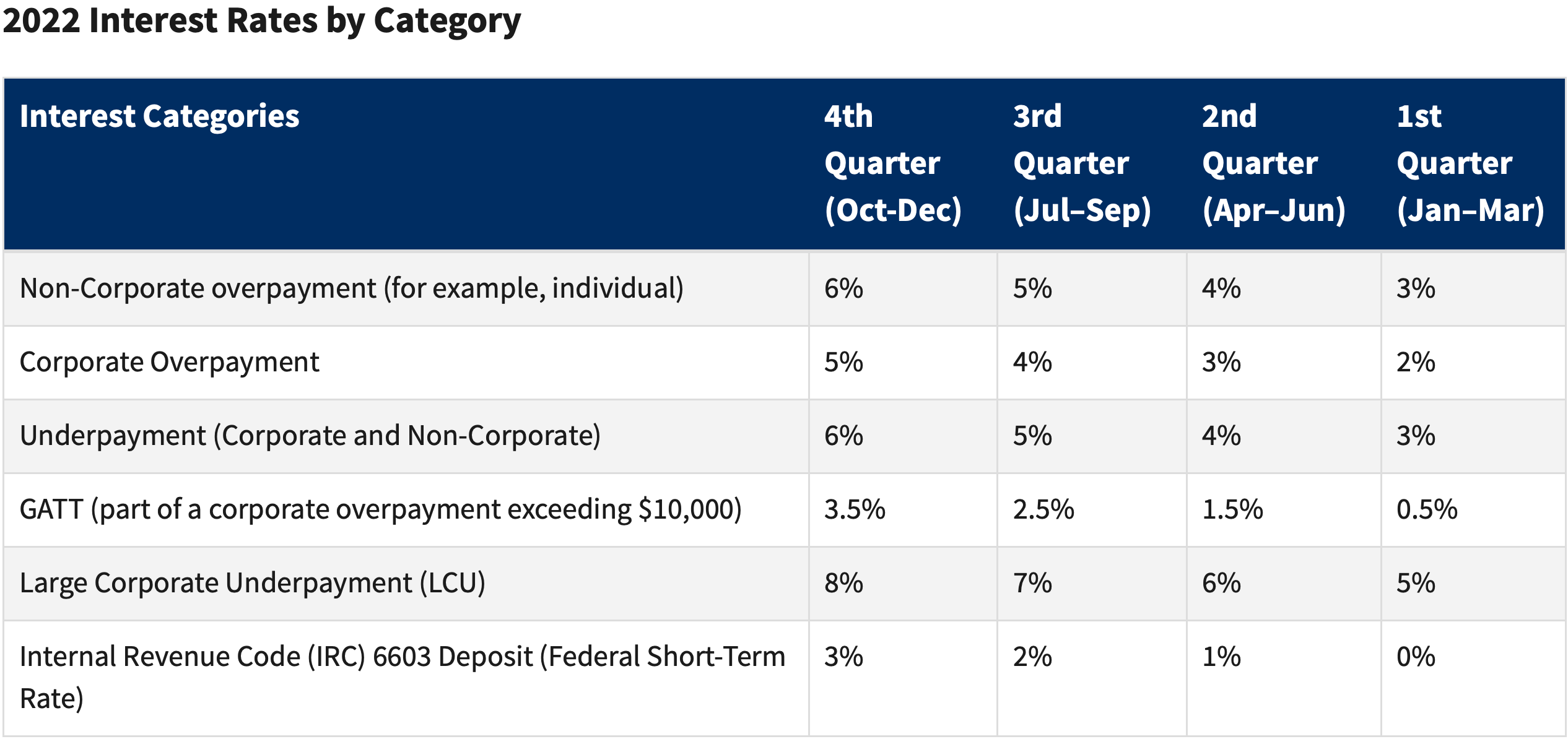

The IRS maintains a website with historical interest rate information. Here is an example from 2022:

The last time the IRS interest rate hit 7% was in the 1st quarter of 2008; since then, rates have generally been in the 3% to 4% range, with some short-term increases to 5% to 6%.

Extension payments. Any tax return balance due must be full-paid by the unextended due date; otherwise, interest and the §6651(a)(2) failure to pay penalty apply to the balance due until it is paid.

Let’s look at three scenarios for a $10,000 Form 1040 balance due not paid until October 15th:

If the 2020 Form 1040 was due on April 15, 2021 (remember, this was actually postponed), the total accruals are $452: $300 for the failure to pay penalty and $152 in interest.

For the 2021 Form 1040, due April 15, 2022, the total accruals are $537: $300 for the failure to pay penalty and $237 in interest.

For the 2022 Form 1040, due April 15, 2023, the total accruals are $657: $300 for the failure to pay penalty and $357 in interest. This assumes the IRS interest rate remains at 7% for the remainder of 2023.

While the failure to pay penalty can easily be removed if First Time Abate applies, interest is rarely abatable, and certainly not in this circumstance.

There is value in the proper calculation of extension payments. How are you providing this service to the client, and how are you charging for it?

Estimated tax payments. The §6654 failure to pay estimated tax penalty for individuals is actually an interest charge — it is the interest due on the missed required estimated tax amount calculated through the due date of the return. Therefore, the IRS interest rate increase will also increase the failure to pay estimated tax penalties.

Let’s look at three scenarios for a $10,000 estimated tax payment requirement, at $2,500 per payment that is unpaid:

For the 2021 Form 1040, the underpayment penalty is $206.

The underpayment penalty for the 2022 Form 1040 is $410, assuming the interest rate is 7% for the 2nd quarter of 2023.

The underpayment penalty for the 2023 Form 1040 is $481, assuming the interest rate is 7% for all relevant periods.

Taxes should not be significantly overpaid; I recommend paying the absolute minimum to avoid the estimated tax penalty and earning interest or other returns on those amounts until the latest payment date possible. I have seen taxpayers lose hundreds, and even thousands, of dollars per year in estimated tax penalties simply because of insufficient withholding or estimated tax payments.

There is value in the proper calculation of estimated tax payments. How are you providing this service to the client, and how are you charging for it?

Taxpayers with unpaid tax debts. Significant and increasing interest accruals are a barrier to taxpayers with unpaid taxes and limited income or assets from fully paying their tax liabilities.

Taxpayers should consider paying off unpaid tax debts as soon as possible to limit accruals at higher interest rates. This may require using cash earning lower than a 7% interest rate or assets appreciating at a rate lower than 7%, even if the taxpayer qualifies to pay the IRS in longer installments. A long-term installment agreement equals a much larger total amount paid to the IRS (with penalty and interest accruals) when compared to a lump-sum payment or short-term installment agreement.

A taxpayer with a pending tax controversy can make a deposit under §6603 to suspend interest accruals. The payment is refundable if none or some of the tax contemplated was ultimately assessed. Rev. Proc. 2005-18 provides the only guidance related to §6603 deposits.

Related to §6603 deposits, if a taxpayer is planning to submit an amended return showing additional tax, the taxpayer should calculate the tax due, plus interest accruals, and remit payment to the IRS as soon as possible to minimize interest accruals and the overall financial impact of the amended return.

There is value in reducing or decreasing interest charges. Are you providing this service to the client, and how are you charging for it if you are?

Refund claims. Any refund claims not processed within 45 days accrue interest payable to the taxpayer. Now that the IRS interest is at 7% and may go higher, there is no urgency for the IRS to process the claim, provided the taxpayer does not need the tax refund. Let the IRS take all the time it needs and have your client enjoy a competitive return on those refund amounts!

Interest Calculation Tools

I recommend TaxInterest to calculate IRS (and state!) interest and penalty accruals. It is an invaluable tool in doing IRS representation work.

I always verify IRS interest and penalty calculations using TaxInterest.

Share Your Thoughts!

If you are a paid subscriber, you can use the comments section below to discuss the tax impacts of higher interest rates.

2023 Compass Tax Educators All-Access Pass

Join Compass Tax Educators for its 2023 live webinar season! I’m the primary instructor, and we have some great classes lined up for 2023.

The 2023 ComPASS provides the following:

Attendance at all LIVE webinars scheduled through December 31, 2023

Minimum 30 scheduled CPE/CE (including 2 hours of Circular 230 ethics and 6 hours of federal tax update)

Any breaking news events held during 2023

Complimentary REPLAY access to all events attended

ON-DEMAND access for all live webinars missed

If you purchase by January 31, 2023, you will receive LIVE attendance to my 8 Tax Season Support Sessions. If you are buying later, you receive REPLAY access to these sessions. These one-hour sessions feature a brief discussion by the instructor and a Q&A period with questions from those who attend live. The Tax Season Support Sessions do not qualify for CPE/CE.

Purchase a 2023 ComPASS by clicking here today!

Canceled tax debt is not COD income; there is authority on that I don’t have on top of mind.

Tom;

1.The question's not about interest rates.

2.I just closed a 2004-2011 CSED case and the IRS "wrote off the balance due' for each year [~~$60K]". I'm presuming there won't be a F1099-C in my client's future. My reading of Tax Topic 431 confirms my presumption. I'd appreciate your opinion.

Thanks,

Gene