Tom Talks Taxes - February 10, 2023

Explaining the new Form 1098-F plus an IRS update on the taxation of state payments

Surprise! The IRS launched a new form in the 1098 series for tax year 2022: Form 1098-F, Fines, Penalties, and Other Amounts. Before getting into what this form reports, let’s go back to our favorite tax law: the Tax Cuts and Jobs Act (TCJA).

Before TCJA, existing §162(f) generally denied a deduction for fines or penalties paid to the government for violating any law.

Revised §162(f)(1) expands the denial of a deduction to any amount paid or incurred (whether by suit, agreement, or otherwise) to, or at the direction of, a government or governmental entity in relation to the violation of any law or the investigation or inquiry by such government or entity into the potential violation of any law. There are exceptions for restitution payments, remediation payments, payments to come into compliance with the law, and any amount paid as taxes due.

At the same time, Congress added §6050X to the Code to create a reporting requirement for amounts potentially subject to §162(f). An information return must be filed with the IRS by a government or governmental entity involved in a suit or agreement stating:

The amount required to be paid as a result of the suit or agreement to which §162(f)(1) applies,

Any amount required to be paid as a result of the suit or agreement which constitutes restitution or remediation of property, and

Any amount required to be paid as a result of the suit or agreement for the purpose of coming into compliance with any law which was violated or involved in the investigation or inquiry.

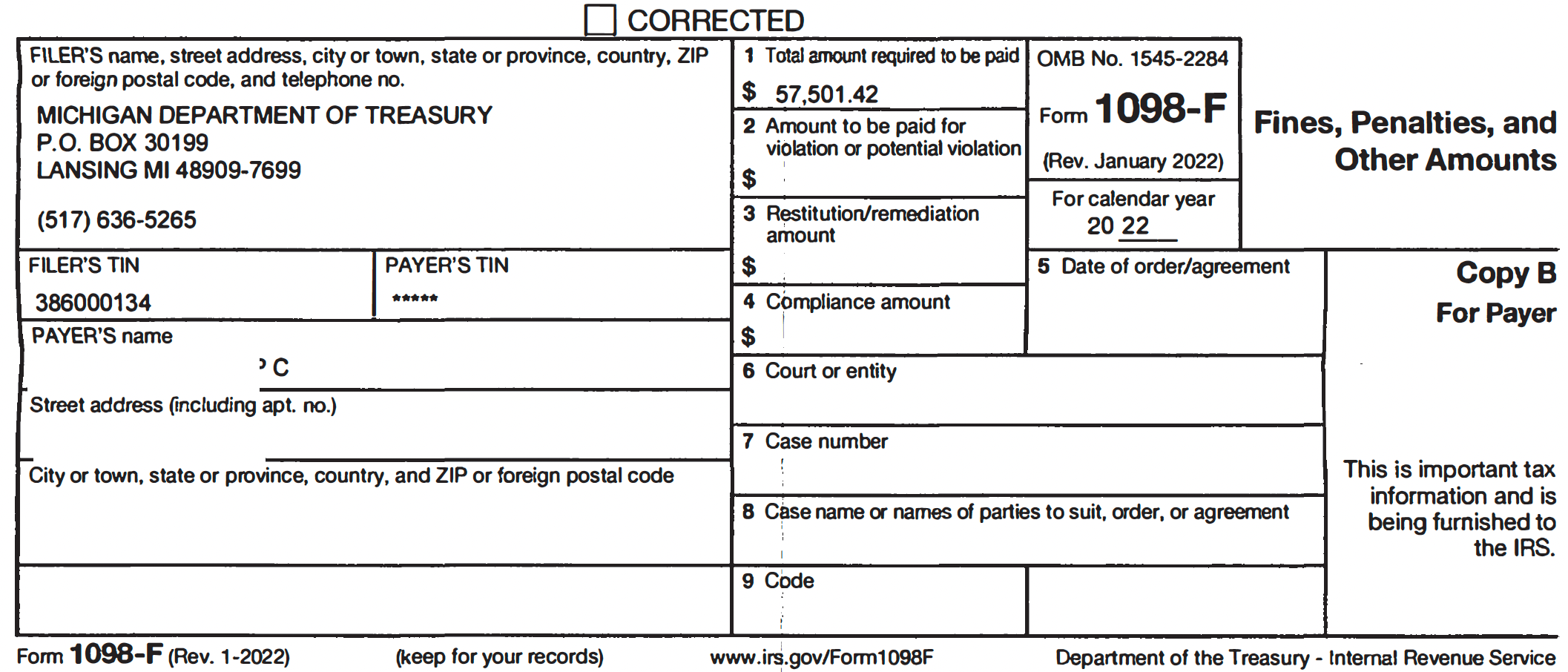

§6050X sets the reporting threshold at $600 but permits the Treasury Secretary to set a higher level. Treas. Reg. §1.6050X-1(f)(6) sets the threshold to $50,000. Here is an example of a 2022 Form 1098-F:

The IRS provided a useful example of Form 1098-F in the 2022 instructions:

Corporation A enters into an agreement with State Y's environmental enforcement agency (Agency) for violating state environmental laws. Pursuant to the agreement, Corp. A pays $40,000 to Agency in civil penalties, $80,000 in restitution for the environmental harm that the Corp. A has caused, $50,000 for remediation of contaminated sites, and $60,000 to conduct comprehensive upgrades to Corp. A's operations to come into compliance with the state environmental laws. Pursuant to the settlement agreement, the aggregate amount Corp. A is required to pay to, or at the direction of Agency, for the violation or potential violation of State Y law exceeds $50,000. Therefore, an appropriate government official of Agency must file Form 1098-F. Agency will complete the Form 1098-F as follows:

Box 1. Total Amount To Be Paid Pursuant to the Suit, Order, or Agreement. Total Amount $230,000 ($40,000 + $80,000 + $50,000 + $60,000)

Box 2. Amount To Be Paid for Violation or Potential Violation $40,000

Box 3. Restitution/Remediation Amount $130,000 ($80,000 + $50,000)

Box 4. Compliance Amount $60,000

In this example, Corporation A may be able to deduct $190,000 (boxes 3 and 4), while $40,000 (box 2) is nondeductible under §162(f)(1). The tax year(s) in which these amounts are recognized depends on when the payments are made and Corporation A’s accounting method (cash or accrual basis).

It is important to note that states are issuing Form 1098-F for unpaid tax balances if penalties were asserted and the total balance owed exceeds $50,000. The Texas Comptroller has a webpage discussing its Form 1098-F policies. From that website:

Michigan posted the following alert on its main tax website:

Please note that this form does not report payments actually made; it reports amounts required to be paid pursuant to a suit, order, or agreement. As such, some, all, or none of the reported amounts may have to be reflected on the tax return for the tax year for which it is issued. If issued to a business, the unpaid amount may reflect a liability property reported on the balance sheet.

State Payment Taxation Update

On its website, the IRS provided informal information on the taxability of various state relief payments during tax year 2022.

For the following states, the IRS stated the 2022 payments issued are refunds of taxes paid and are excluded from income under §111 unless the recipient received a tax benefit in the year the taxes were deducted:

Georgia

Massachusetts

South Carolina

Virginia

For the following states, the IRS stated it will not challenge the position, either on an original or amended return, that the 2022 payments issued are excluded from income either under the general welfare exclusion or the §139 qualified disaster relief payment exclusion:

Alaska (not including the annual Permanent Fund Dividend)

California

Colorado

Connecticut

Delaware

Florida

Hawaii

Idaho

Illinois

Indiana

Maine

New Jersey

New Mexico

New York

Oregon

Pennsylvania

Rhode Island

Illinois and New York issued multiple payments and in each case one of the payments was a refund of taxes, which should be treated as noted above, and one of the payments is in the category of disaster relief payment.

In this prior edition, we explained how to apply the §111 tax benefit rule, the general welfare exclusion, and the §139 qualified disaster relief payment exclusion to state relief payments.

If a taxpayer receives a Form 1099-MISC for a payment listed in the second grouping above, including the California Middle Class Tax Refund, it should be reported on Schedule 1, line 8z, and then subtracted as an adjustment to income on Schedule 1, line 24z using either the general welfare exclusion or the qualified disaster relief payment exclusion.

Share Your Thoughts!

As a paid subscriber, you can discuss Form 1098-F and the federal taxation of state rebates and payments in the comments below.

Thank you - this is quite comprehensive. The most helpful is where to do an adjustment due to this newly popped instruction. Super useful information. Liked the format, too.

No news on the payments in Iowa?