Lump-Sum Social Security Payments Going Out Now

What are the federal tax issues for recipients of the WEP/GPO payments?

On January 5, 2025, President Biden signed the Social Security Fairness Act into law. It ended the Windfall Elimination Provision (WEP) and Government Pension Offset (GPO) retroactively to January 1, 2024.

These provisions reduced or eliminated the Social Security benefits of over 3.2 million people who receive a pension based on work that Social Security did not cover because they did not pay Social Security taxes. These provisions primarily affected teachers, firefighters, police officers, federal employees covered by the Civil Service Retirement System, and people whose work had been covered by a foreign social security system.

Lump-Sum Payment

The Social Security Administration sent retroactive lump-sum payments starting February 25, 2025. These payments are retroactive benefits covering January 2024 through February 2025. Affected beneficiaries will begin receiving their new monthly benefit amount in April 2025 (for their March 2025 benefit).

This lump-sum payment is treated as a Social Security payment. Depending on the taxpayer's situation, it may or may not be taxable; therefore, tax professionals should offer paid assistance to help these taxpayers project the tax due on this payment and make the appropriate tax payments to cover the tax due on that payment.

Social Security benefit taxation is a complex formula, and unfortunately, many of the triggers have not been indexed for inflation, so the dollar amounts are decades old.

Up to 50% of a taxpayer’s Social Security benefits may be taxable if the total of one-half of the benefits paid plus all other gross income (including tax-exempt interest) is between the following amounts by filing status:

$25,000 to $34,000 for single, head of household, or qualifying surviving spouse,

$25,000 to $34,000 for married filing separately if the taxpayer lived apart from their spouse for the entire year, and

$32,000 to $44,000 for married filing jointly.

Up to 85% of a taxpayer’s Social Security benefits may be taxable if the total of one-half of the benefits paid plus all other gross income (including tax-exempt interest) is greater than the following amounts by filing status:

$34,000 for single, head of household, or qualifying surviving spouse,

$34,000 for married filing separately if the taxpayer lived apart from their spouse for the entire year,

$44,000 for married filing jointly, and

$0 for married filing separately if they lived with their spouse at any time during the tax year.

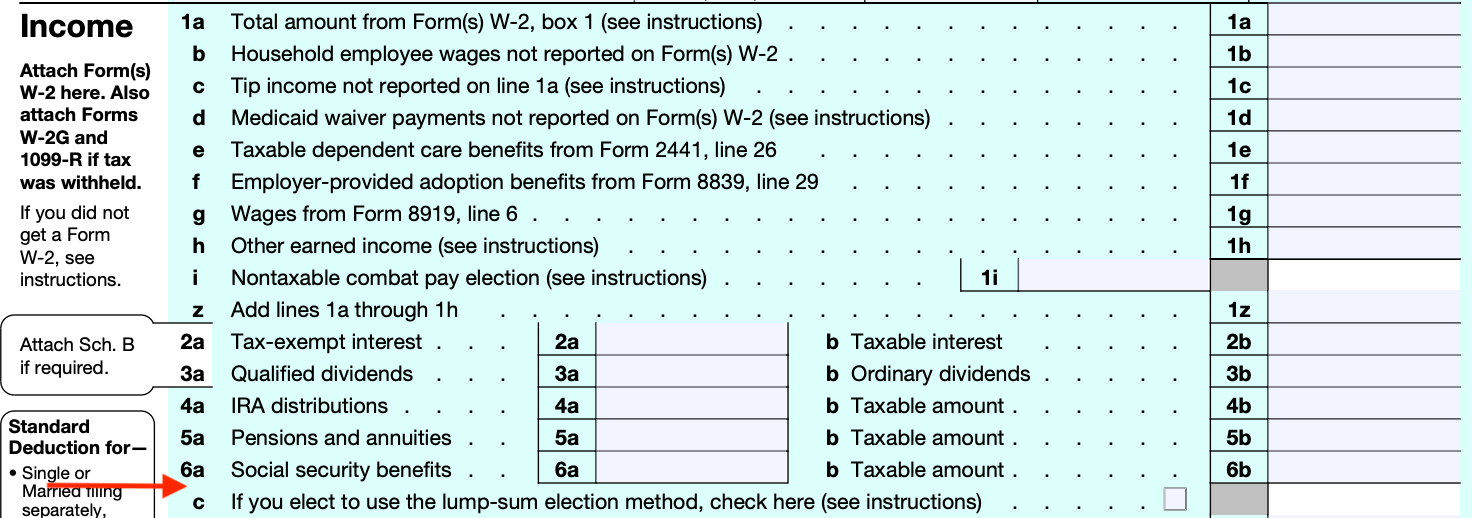

Lump-Sum Election

When a taxpayer receives a lump-sum payment of Social Security benefits attributable to prior tax years, the taxpayer can possibly reduce the taxable portion of that payment by making a lump-sum election under §86(e).

If the lump-sum election is made, the taxable amount is equal to the sum of the amounts that would have been taxable each year if the components of the lump-sum payment were received in the year to which they are attributable. A taxpayer makes the lump-sum election by checking the box on line 6c on Form 1040.

Lump-Sum Election Example

Carlos received a $7,000 WEP/GPO lump-sum payment in 2025. $6,000 of that payment is attributable to 2024, and the remaining $1,000 is attributable to 2025.

If 85% of Carlos’s 2025 Social Security benefits are taxable based on his income and he does not make the lump-sum election, $5,950 of the $7,000 payment will be included in his 2025 gross income.

Assume that including the $6,000 attributable to 2024 on his 2024 return would have made $1,000 of that amount taxable. If Carlos makes the lump-sum election for tax year 2025, he will only include $1,850 of the $7,000 payment in his 2025 gross income ($1,000 attributable to 2024 plus $850 attributable to 2025). Making the lump-sum election reduces Carlos’s 2025 adjusted gross income (AGI) by $4,100.

Join the Conversation

As a paid subscriber, you can discuss this topic in the comments section. Please keep the discussion related to this edition’s topic.

Learn More About Tom

Please take a look at my website to learn about the educational opportunities I offer the tax professional community.

thank you for this - the clarification and simple explanation is SO appreciated!

Thank you some much for the direction